by hitesh parmar | Jun 6, 2021 | News |

Background:

43rd GST council meeting was held on 28th May 2021. People had great expectations from the meet as the country was struggling with Covid-19 pandemic’s second wave.

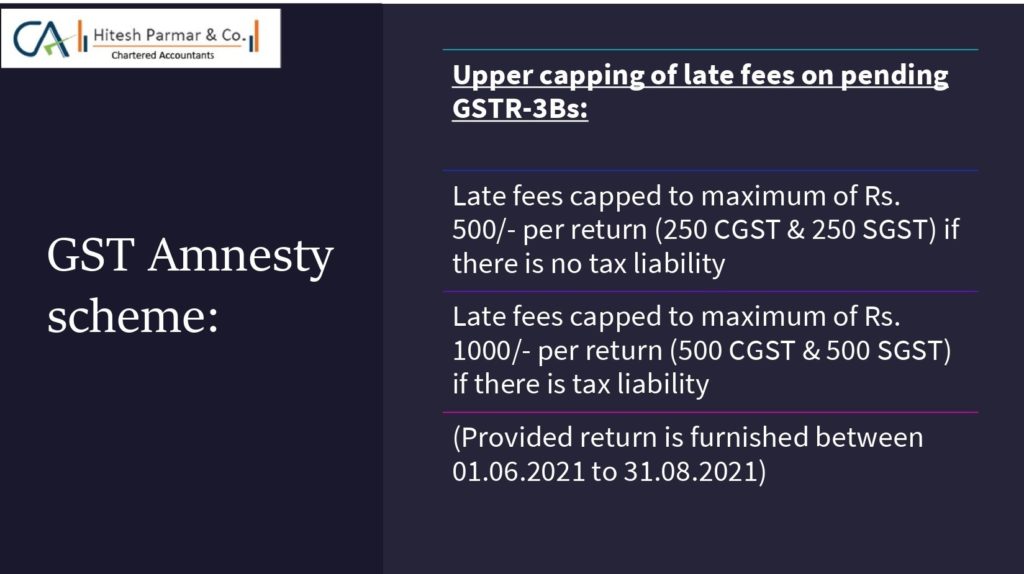

The GST Council recommended to cap the late fees on GSTR 3Bs of Rs.500/- per return or Rs.1000/- per return depending upon whether it is Nil return or not.

One of the important shortcomings of this meet was section 16(4) of the CGST Act on Input Tax credit. Section 16(4) was not discussed at all, which left the already cash strapped taxpayers with burden which is more than the benefit awarded by way of capping of late fees on GSTR-3Bs.

Read on to know more….

As per section 16(4) of CGST Act, 2017, A registered person shall not be allowed to take input credit in respect of any invoice after the due date of furnishing of the GSTR-3B for the month of September after the end of financial year or furnishing of the relevant annual return, whichever is earlier. Thus for,

FY 2017-18: Last date to avail GST Credit was 25th Oct 2018

(Due date of GSTR 3B: 25th Oct 2018 or last date for filing annual return: 31st Jan 2020, whichever is earlier)

FY 2018-19: Last date to avail GST Credit was 20th Oct 2019

(Due date of GSTR 3B: 20th Oct 2019 or last date for filing annual return: 31st Mar 2021, whichever is earlier)

FY 2019-20: Last date to avail GST Credit was 20th Oct 2020

Imagine a person having say, Rs.10 Lakhs of eligible Input tax credit for the above years. He will be denied credit which was legitimately paid by his supplier with the government just because he did not furnish returns on time & now that he is ready to correct his mistake by filing the same along with the applicable late fees, he would not be entitled to his rightful Input tax credit.

Isn’t this double taxation?

Comment your thoughts below. Connect with us to know more!

GST Amnesty scheme as announced in the 43rd GST Council meet

by hitesh parmar | Oct 25, 2020 | News |

The government has announced guidelines for the waiver of compound interest that was payable by borrowers who had opted for moratorium on their loan equated monthly instalments (EMI) between March 1, 2020 and August 31, 2020.

In this article, we have tried to cover all important points about interest rate waiver viz who is eligible, amount of waiver, types of loans covered, time limit till when this benefit shall be credited to the borrowers account etc to enable the borrowers know about their all rights about interest waiver.

More importantly this is available even if the moratorium is not obtained.

Who are eligible?

All borrowers whose loan amount does not exceed Rs 2 crore – aggregate of all the facilities from the lending institutions.

The loan account should be standard account as on February 29, 2020

Types of loan covered?

MSME loans, Education loan, Housing loans, Consumer durable loans, Credit card dues, Automobile loans, Personal loans to professional & Consumption loans.

Loans should be availed from?

The lending institution should be either: Banking company, Public sector bank, Co-operative bank or Regional rural bank, All India Financial Institution, Non-Banking Financial Company or Housing Finance Company.

I did not opt for moratorium, am I covered to this benefit?

The payment will be made to the borrower’s loan account irrespective of whether the borrower has fully availed, partially availed or not availed the moratorium. Thus, even if you have not opted for the moratorium, then also you are eligible under the scheme

Amount of benefit

Under the scheme, the difference between the compound interest and simple interest will be credited to the borrower’s loan account for the period between March 1, 2020 and August 31, 2020

By when I shall get the amount of this benefit?

The lending institution is required to credit the amount to the borrower’s account by November 5, 2020.

Illustration:

| Principal Amount |

85,00,000 |

1,05,00,000 |

1,80,00,000 |

| Interest Rate |

13.50% |

13.50% |

13.50% |

| Int for 6-month moratorium with compound interest(A) |

5,90,130 |

7,28,984 |

12,49,688 |

|

|

|

|

| Int for 6-month moratorium with Simple interest(B) |

5,73,750 |

7,08,750 |

12,15,000 |

|

|

|

|

| Net Refund |

16,380 |

20,234 |

34,688 |

Should you have any query write back to us at:- info@hiteshparmarandco.com

by hitesh parmar | Oct 6, 2020 | News |

Recommendations made:

- Compensation Cess extended beyond the period of 5 years i.e. June, 2022, till the period as may be required to meet the revenue gap

- Due date for furnishing quarterly GSTR-1 for quarterly tax-payers revised to 13th of the month succeeding the quarter w.e.f. 01.01.2021. (Currently the deadline is 11th of the month succeeding the quarter)

- Automation of GSTR-3B

- Auto population of liability from GSTR 1 w.e.f. 01.01.2021

- Auto population of input tax credit from supplier’s GSTR 1 through the newly form GSTR 2B for monthly filers w.e.f. 01.01.2021 and for quarterly filers w.e.f. 01.04.2021

- To ensure auto population of liability and ITC in GSTR 3B, form GSTR-1 would be mandatorily filed before form GSTR 3B w.e.f. 01.04.2021.

- The present GSTR-1/3B to be extended till 31.03.2021 and the GST Laws to be amended to make the GSTR-1/3B return filing system as the default return filing system.

- Reducing compliance burden for small tax-payer

- Small taxpayers having aggregate annual turnover < Rs. 5 Cr would be allowed to file quarterly returns with the monthly payment requirements. Such quarterly taxpayers would, for the first two months of the quarter, have an option to pay 35% of the net cash tax liability of the last quarter using an auto-generated challan. (w.e.f. 01.01.2021)

- Revised HSN and SAC requirements

- HSN/SAC of 6 digits required for taxpayers with aggregate annual turnover above 5 Crores

- HSN/SAC of 4 digits required for B2B supplies for taxpayers with aggregate annual turnover upto 5 Crores

- Government to have power to notify 8 digit HSN code on notified class of supplies by all taxpayers

- Other misc. recommendations

- Various changes in the CGST Rules and forms have been recommended which includes provision for furnishing of NIL Form CMP-08 through SMS.

- Refund to be paid in a validated bank account linked with the PAN & Aadhar of the registrant w.e.f. 01.01.2021.

- To encourage domestic launching of satellites particularly by young start-ups, the satellite launch services supplied by ISRO, Antrix Corporation Ltd. & NSIL would be exempted.

Summary: Seeing at the recommendations of the 42nd council meet, the government is trying to make the GST laws including the system more system based & automated & thereby reduce the human errors, duplication/ ineligible claim of input tax credit.

Note: The decisions of the GST Council have been presented in this note in simple language for easy understanding. The same would be given effect to through Gazette notifications/circulars which alone shall have force of law.

For any query related to GST write back to us at:- info@hiteshparmarandco.com

by hpacadmin | Sep 28, 2020 | News |

Through Order Case No.4 of 2017, dated 8th September 2017 the Maharashtra Real Estate Regulatory Authority has passed an order apropos Online Applications received after 16th August 2017 for Registration of Ongoing Projects.

Synopsis of the Order

The Maharashtra Real Estate Regulatory fixed the amount of penalty for non-registration of on-going projects based on the date of receipt of an application for registration.