Background:

43rd GST council meeting was held on 28th May 2021. People had great expectations from the meet as the country was struggling with Covid-19 pandemic’s second wave.

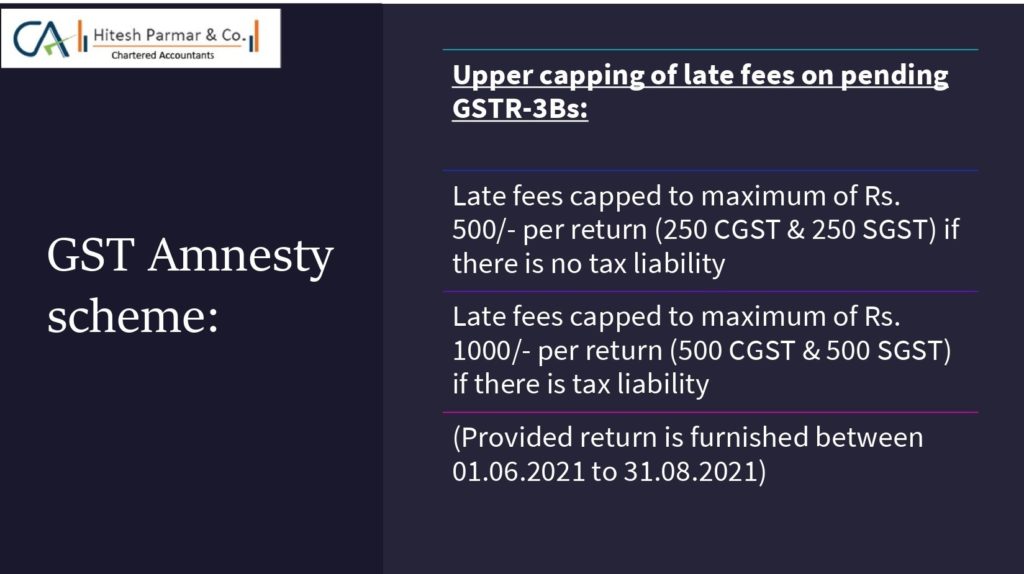

The GST Council recommended to cap the late fees on GSTR 3Bs of Rs.500/- per return or Rs.1000/- per return depending upon whether it is Nil return or not.

One of the important shortcomings of this meet was section 16(4) of the CGST Act on Input Tax credit. Section 16(4) was not discussed at all, which left the already cash strapped taxpayers with burden which is more than the benefit awarded by way of capping of late fees on GSTR-3Bs.

Read on to know more….

As per section 16(4) of CGST Act, 2017, A registered person shall not be allowed to take input credit in respect of any invoice after the due date of furnishing of the GSTR-3B for the month of September after the end of financial year or furnishing of the relevant annual return, whichever is earlier. Thus for,

FY 2017-18: Last date to avail GST Credit was 25th Oct 2018

(Due date of GSTR 3B: 25th Oct 2018 or last date for filing annual return: 31st Jan 2020, whichever is earlier)

FY 2018-19: Last date to avail GST Credit was 20th Oct 2019

(Due date of GSTR 3B: 20th Oct 2019 or last date for filing annual return: 31st Mar 2021, whichever is earlier)

FY 2019-20: Last date to avail GST Credit was 20th Oct 2020

Imagine a person having say, Rs.10 Lakhs of eligible Input tax credit for the above years. He will be denied credit which was legitimately paid by his supplier with the government just because he did not furnish returns on time & now that he is ready to correct his mistake by filing the same along with the applicable late fees, he would not be entitled to his rightful Input tax credit.

Isn’t this double taxation?

Comment your thoughts below. Connect with us to know more!

GST Amnesty scheme as announced in the 43rd GST Council meet